Positive passenger traffic and financial trends amid macroeconomic impact: ACI Asia-Pacific & Middle East

- 2024-02-15

Asia-Pacific and the Middle East region is expected to return as engine of global economic growth in 2024

The Airports Council International Asia-Pacific & Middle East’s (ACI APAC & MID) latest Airport Industry Outlook provides a positive trend into the recovery of passenger traffic and airport finances, but macro-economic factors still pose a challenge for the overall recovery of the sector.

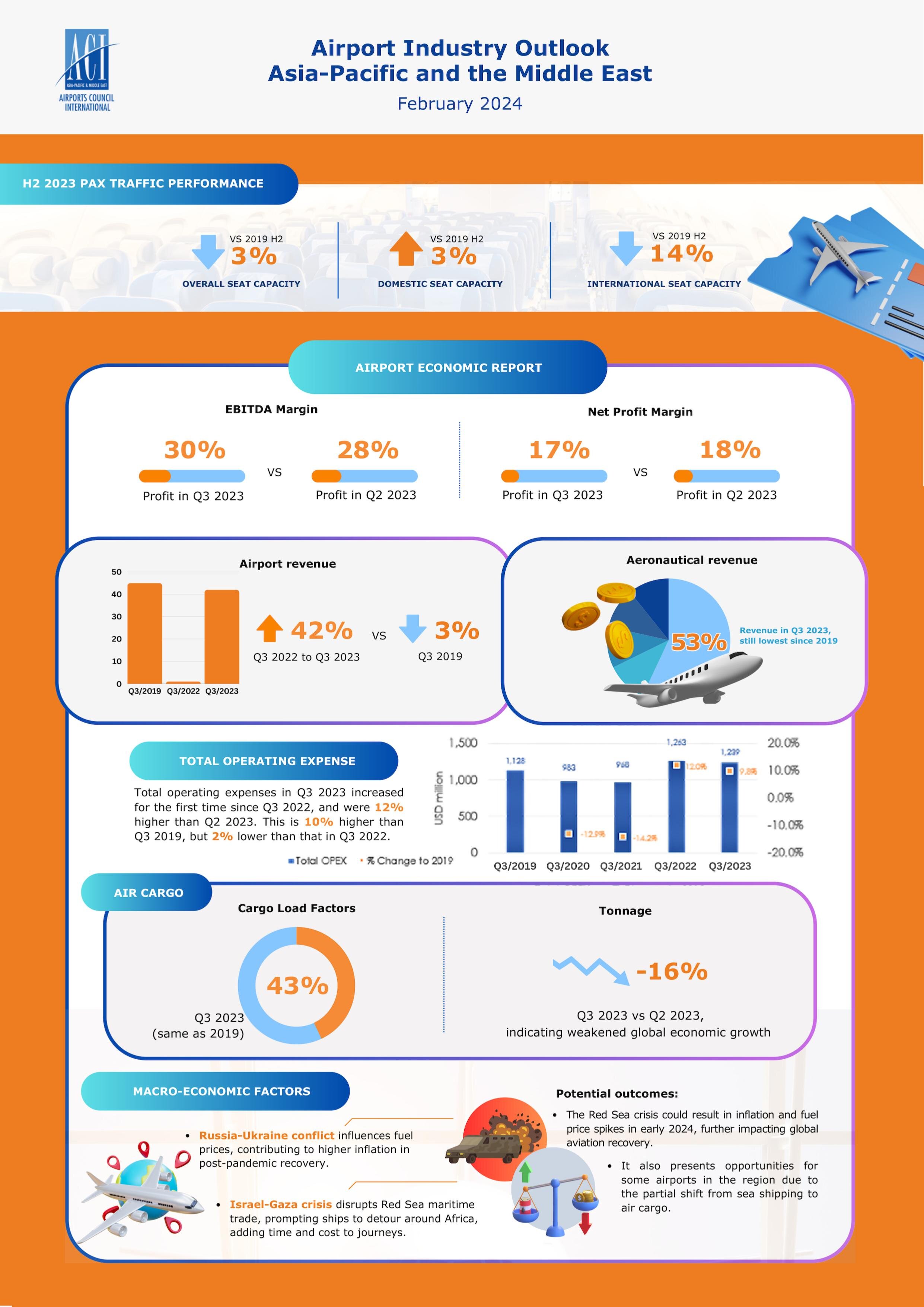

The Airport Industry Outlook, developed in partnership with Mott MacDonald, reveals the overall seat capacity in H2 2023 is just 3% below the levels recorded in 2019 H2. While the domestic seat capacity in H2 2023 grew by +3% over the same period in 2019 but international is lagging at -14%.

After a positive beginning to the year 2023, with China fully reopening the borders, the overall traffic in Asia-Pacific has rebounded to almost 90% of the pre-pandemic levels, the Middle East stood out, recording a growth of nearly +4% compared to the 2019 figure. The outlook for 2024 remains positive, with the expectation of a full recovery of the Asia-Pacific region in 2024. Over the same year, the Middle East is expected to confirm its trajectory of growth with a record year above 450 million passengers. Asia-Pacific and the Middle East should look at the future with cautious optimism.

Geopolitical tensions in Eastern Europe and in the Middle East are a matter of concern, especially if they will be protracted for a long period and require a high degree of adaptability. The Red Sea crisis is no exception, a vital route for international shipping, has forced many ships to reroute around Africa, extending both time and expense for their journeys. As such, shippers may seek to switch to air cargo, prompting airlines to potentially raise air cargo rates. On the other hand, the stimulating demand for air cargo may prove to be an advantage for airports, particularly in Asia and the Middle East, and Europe.

Cargo load factors (CLFs) remained steady at 43% in Q3 2023, comparable to pre-pandemic levels of 46% in 2019 (full year) but below the peak of 58% in Q1 2021. Notably, Asia-Pacific CLFs surpassed the global average, increasing from 44% in Q2 2023 to 46% in Q3 2023, although still lower than the 2021 full-year average of 66%. Meanwhile, Middle East CLFs, marginally below the global average, decreased from 43% in Q2 2023 to 41% in Q3 2023.

Analysing the trends, Mr. Stefano Baronci, Director General of ACI Asia-Pacific & Middle East, said, “As reported by the International Monetary Fund, overall, Asia is on track to deliver two-thirds of global growth in 2024 and remains the key engine of economic growth in the World. This is reflected in the consistent positive trends in traffic and finances with airports in our region, which in 2024 is expected to reach a market share of almost 40% of the total passenger and cargo traffic at global level. From 2024 onwards, we hope that the expression “pre-COVID recovery” with reference to Asia will soon become obsolete in our vocabulary. While still navigating macroeconomic and geopolitical risks, we remain optimistic about growth prospects in the region, with our estimates suggesting Asia-Pacific to record 3% growth and the Middle East to consolidate its upward trajectory with a growth of 14% over 2019 levels.”

Airport Economics

Traffic growth continued in Q3 2023, and airports in the APAC and ME regions continued to operate profitably. Overall, the EBITDA margins for Q3 2023 increased to 30% from 28% in Q2 2023. However, the net profit margins decreased marginally from 18% in Q2 2023 to 17% in Q3 2023.

While airport revenues saw a 42% improvement from Q3 2022 to Q3 2023, they remain -3% below Q3 2019. Aeronautical revenue accounted for 53% of total revenue in Q3 2023, marking the lowest since 2019. Additionally, total operating expenses increased for the first time since Q3 2022, rising by 12% compared to Q2 2023 and 10% higher than Q3 2019.

In Q3 2023, total operating expenses registered the first increase since Q3 2022, marking a 12% rise from Q2 2023. While this figure is 10% higher than Q3 2019, it is 2% lower than the total operating expenses in Q3 2022. The surge in labor and energy costs, driven by the recovery in traffic, is likely a contributing factor to this increase.

The Report is available for download for members only. Download your copy!

- CATEGORY

- COUNTRY / AREA

- Hong Kong SAR

- AUTHOR

- ACI Asia-Pacific & Middle East

RELATED NEWS

- 2025-10-09

- Press Release

Asia-Pacific and Middle East witness sharp airfare increase

- 2025-05-12

- Press Release

Asia-Pacific and Middle East Airports commits to capacity optimisation and infrastructure upgrades-- both on ground and in the air