Middle East airports under stress as geopolitical conflict disrupts air transport in Asia-Pacific but traffic remains resilient

- 2026-05-13

Airports Council International Asia-Pacific & Middle East (ACI APAC & MID), the association representing more than 600 airports across 45 countries and territories, today released a comprehensive assessment of the operational and economic impact of the ongoing military conflict in the Gulf on regional aviation infrastructure in Middle East.

The assessment, conducted in partnership with Flare Aviation Consulting, covers the two-month period from the conflict's onset through 30 April 2026. It confirms that the military conflict has pushed the global air transport network under acute stress, with Middle East airports bearing a disproportionate and sustained burden due to its role as one of the world’s most important transport corridors linking Europe, Asia, Africa, and the Americas.

The nine airports in this study collectively handled 324 million passengers in 2025, i.e. about 70% of the total traffic in the Middle East over the same year, and disruptions in this corridor have consequences across the global aviation network.

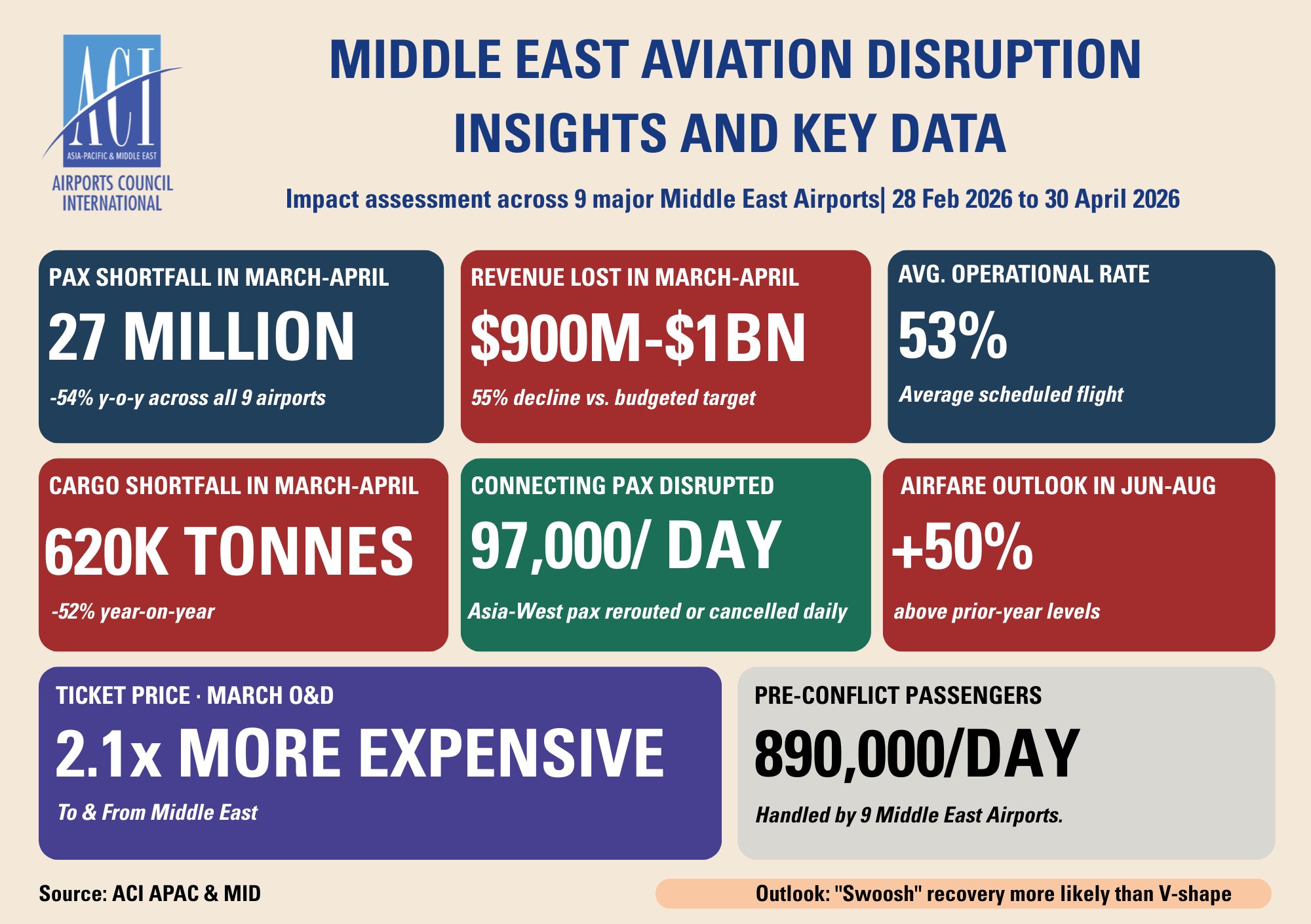

The nine airports, operated at an average of just 53% of pre-conflict scheduled flights across March and April 2026. Operations fell to as low as 32% of scheduled capacity on the first day of the conflict, before partially recovering to approximately 63% by the final week of April, evidence of the capacity of the system to absorb significant disruption while maintaining overall operational continuity.

In 2025, approximately 197 million passengers travelled between Asia-Pacific and western destinations (Europe, Americas and Africa) equivalent to 540,000 passengers daily, with 18% of those, or roughly 97,000 passengers per day, connecting through the affected hubs in the Middle East. The restriction of Gulf airspace effectively removed nearly one-fifth of all East-West connecting capacity from the global aviation network within hours of the conflict's onset, an event of systemic significance for international air transport.

Financial Damage

The revenue shortfall incurred by these nine airports over the two-month period is estimated at US$900 million to 1 billion, set against a budgeted revenue target of US$1.3-1.4 billion for the same period. This represents a shortfall equivalent to 55% of anticipated revenues, a loss of exceptional magnitude for an industry characterised by regulated margins, fixed cost structures, and long-term capital commitments tied to infrastructure programmes.

The revenue shortfall sustained by airports is attributable to the collapse in passenger and cargo volumes.

The financial impact constitutes a structural cash flow challenge for hub operators, many of whom carry significant fixed cost obligations in support of long-term infrastructure investment programmes.

Scale of loss

An estimated 27 million passengers across the nine airports did not travel as planned during March and April 2026, representing a year-on-year decline of 54%. March recorded the most acute impact, with 14 million passengers lost, a 57% year-on-year reduction, followed by a further 13 million in April, representing a 50% decline compared to the same period in 2025.

Cargo operations sustained equally severe disruption. The nine airports are estimated to have collectively handled 571,000 tonnes of freight across the two-month period, against 1.19 million tonnes in the corresponding period of 2025, a loss of approximately 620,000 tonnes, or 52% year-on-year. March represented the most severe month for cargo, with volumes down 59% year-on-year at 259,000 tonnes. April showed early indications of partial recovery, with 312,000 tonnes handled, still 43% below the prior-year level.

Elevated air fares

The disruption has been particularly evident on Asia-West (Europe, Americas and Africa) long-haul routes. Direct fares, once priced at a modest 20% premium over indirect routings via the Middle East, more than doubled in March, reaching 185% of the 2025 indirect-via-Middle East baseline.

Even by July-August, airfares to and from Middle East were priced at an average of 50% above pre-conflict levels. The primary driver behind these increases is reduced airline competition, as East-West traffic flows have shifted heavily towards European and Asian carriers, limiting capacity and pushing prices upward. Looking ahead, airfares are expected to stay elevated in the short to medium term as market imbalances and cost pressures persist.

Airport charges unchanged

This rise in airfares is evidence of how the imbalance between supply and demand drives prices upward. On the contrary, airport charges, which are regulated instruments subject to established regulatory frameworks, remained unchanged throughout this period and have not contributed to the elevated airfares observed across affected markets. Given the current capacity constraints and rising passenger volumes across Asia-Pacific and the Middle East, airports must prioritise committed capital expenditure to ensure operational continuity and prepare for the decades of growth ahead. The region served 3.9 billion passengers in 2024 and is projected to exceed 11 billion by 2054. The capital investment required to bridge that gap cannot be deferred.

Rising fuel prices challenge airports despite stable stock

Despite the disruption in the Middle East, overall passenger traffic in Asia-Pacific remained resilient and in upward trend in March at most of the airports surveyed, although airports experienced declines on the routes to the Middle East. According to an ACI Asia-Pacific & Middle East survey, covering 28 major airport operators, the rising jet fuel prices, rather than physical shortages, are the main challenge facing airports. While fuel stocks remain stable, for the majority of airports market conditions are tightening, with jet fuel prices remaining nearly double pre-conflict levels.

Many airports have introduced mitigation measures, including contingency planning, supplier coordination, and reserve stocking, while government support remains limited. ACI APAC & MID cautions that the next few months will be critical and called on airports and governments to strengthen fuel security measures, improve contingency planning, and diversify fuel-supply chains to reduce single-region dependency.

Stefano Baronci, Director General, ACI Asia-Pacific & Middle East, said: “Middle Eastern hubs are not only regional assets but essential nodes in the global aviation system. The scale of disruption observed over two months underscores the critical role of airports as enablers of connectivity, socio-economic growth, and passenger experience. The aviation ecosystem in Asia-Pacific and Middle East is proving to be resilient, but we are at a critical juncture, since a protracted instability over the summer period may have far more negative impact of the economic sustainability of the airport sector. Against a backdrop of renewed upward pressure on jet fuel prices, longer routings driven by geopolitical tensions, persistent supply bottlenecks, and chronically elevated inflation, public policy should not add yet another layer of cost to air travel. Further increases in government-imposed taxes, such as the latest taxation applied to passengers departing Australia, directly undermine connectivity, tourism, trade and consumer welfare.”

Outlook

Recovery is expected to follow a gradual “swoosh-shaped” trajectory--- a slow initial rebound followed by a longer, gradual climb back to baseline -- rather than a rapid rebound. Continued airspace restrictions, security risks, and elevated fuel prices are likely to weigh on demand and airline capacity. The pace of recovery will depend on coordinated airspace reopening, clearer regulatory guidance, stabilisation of fuel markets, and the ability of Middle Eastern carriers to rebuild networks and restore passenger confidence.

- CATEGORY

- COUNTRY / AREA

- Hong Kong SAR

- AUTHOR

- ACI Asia-Pacific & Middle East

RELATED NEWS

- 2023-03-02

- Members’ News

Bahrain Airport Company and Airports Council International Reveal Global Aviation Industry is on Track for Stronger Recovery in 2023

- 2022-11-24

- Press Release

Aviation Recovery Continues Despite Challenges: ACI Asia-Pacific Q3 Airport Industry Outlook